{kind=link}

It has been 15 years since I first addressed why the “Wealth Impact” is a straightforward correlation error:

“The essential premise of the wealth impact is well-known: As the worth of inventory portfolios rise throughout bull markets, buyers take pleasure in a sense of euphoria. This psychological state makes them really feel extra snug — about their wealth, about debt, and most of all, about spending and indulgences. The online outcome, goes the argument, is that customers spend extra, stimulate the financial system, thus resulting in extra jobs and tax revenues. A virtuous cycle is created. The issue is, the speculation is generally nonsense.” The Massive Image, Nov 16, 2010

It’s superb that the Federal Reserve continues to make coverage based mostly on what I argue is a elementary misunderstanding of each economics and psychology.

No, spending doesn’t go up as a result of shares are up; quite, the components that underpin increased shopper spending – will increase in employment, wages, credit score, and even modest inflation, plus the rest underpinning financial growth1 – are likely to additionally drive up revenues, income, investor sentiment, and due to this fact inventory costs.2

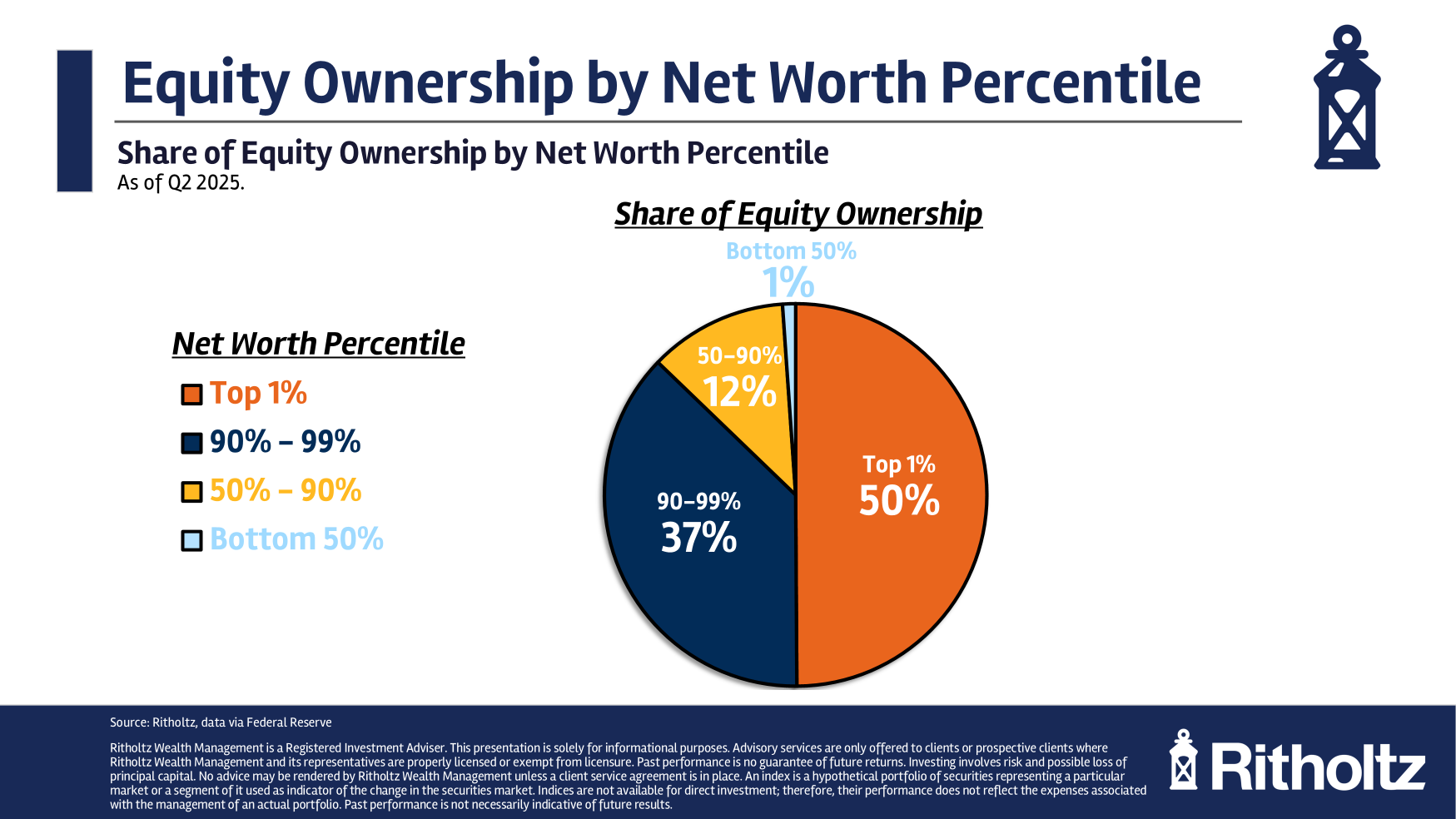

However that’s solely the primary half of the Wealth Impact conundrum; the opposite half is that most individuals within the nation personal little or no in equities. You’ve got seen the information earlier than: The highest 10% personal 87% of the inventory market whereas the underside 90% personal simply 13%.

Does anybody actually consider the inventory market is what drives spending for the 90% who solely personal 13% of equities?

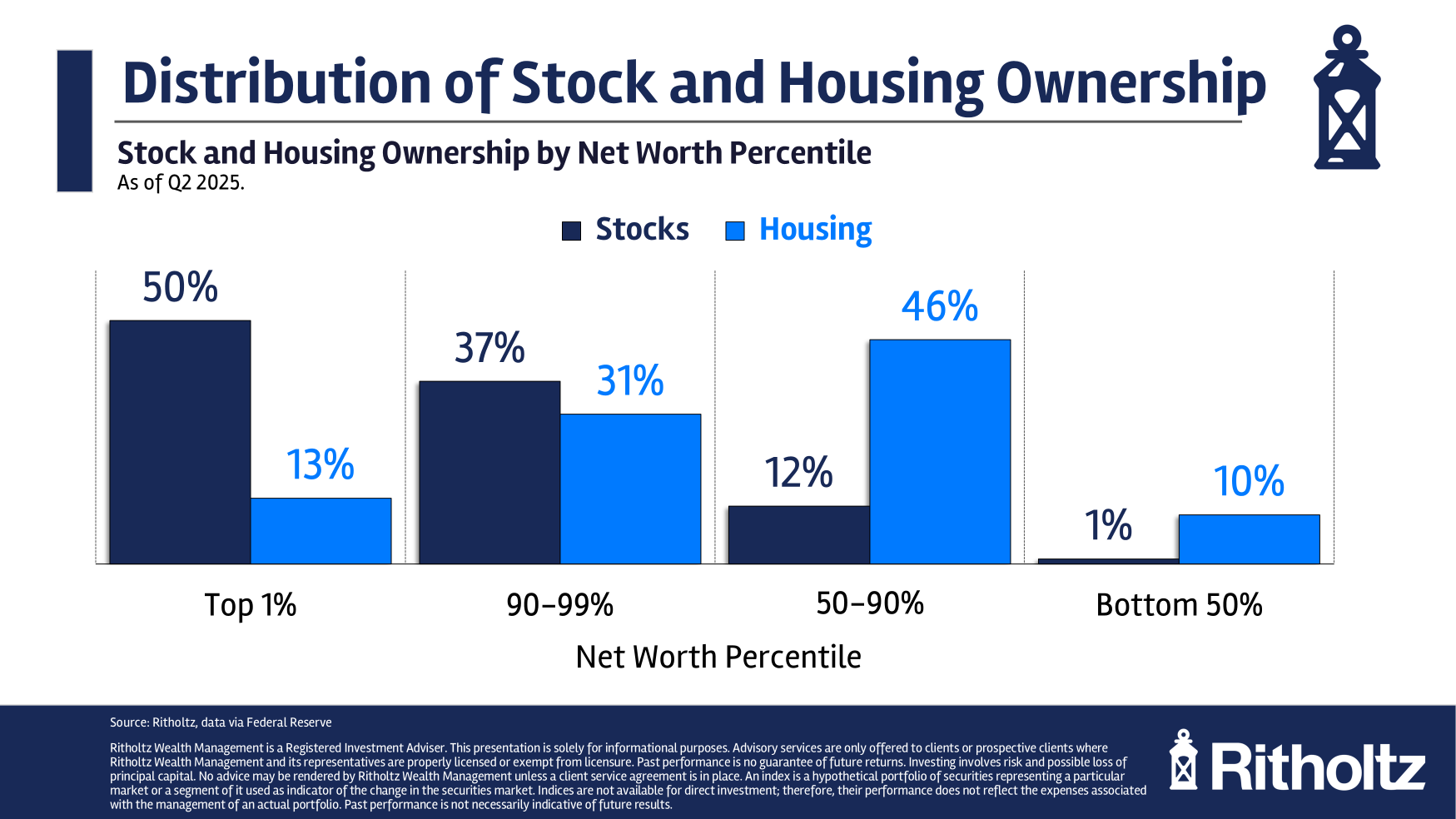

There IS an actual wealth impact with housing – the underside 90% personal 87% of the homes – fairly near what you anticipate. However even these numbers are skewed; the decrease half of households – AKA renters – solely personal 10% of the housing inventory. So even the wealth impact of housing is considerably muted.

What actually drives shopper spending increased?

Plentiful jobs, wage will increase, financial growth, labor mobility, and bountiful credit score availability have defined the previous habits of customers. It isn’t a secular bull market in shares that causes shopper spending to extend; it’s the similar contemporaneous components that energy a bull market that additionally drive spending.

If anybody has persuasive knowledge displaying that fairness bull markets create an actual wealth impact that’s greater than a correlation, and is genuinely causative, I’d like to see it…

Beforehand:

Wealth Impact is a Dangerous Correlation Fantasy (April 25, 2016)

Fed is Too Targeted on Wealth Impact, Fairness Markets (February 6, 2014)

Wealth Impact Rumors Have Been Drastically Exaggerated (November 16, 2010)

See additionally:

Financial system Wall Road has a shopper spending drawback (AxiosSeptember 9, 2025)

Rich People Are Spending. Individuals With Much less Are Struggling. (New York InstancesOctober, 19, 2025)

Updates weekly U.S. Shopper Confidence Tracker (Morning Seek the advice ofOctober, 20, 2025)

Washington Could Be Lacking Indicators of Financial Hassle: Why Republicans and Democrats alike get fooled by the inventory market. (PoliticoOctober 21, 2025)

__________

1. You possibly can add one other wrinkle to the causation correlation concern: The reversal of extraordinary spending patterns in items versus companies through the pandemic, adopted by the eventual return to close regular previously few years…

2. I’ve mentioned beforehand that almost all sentiment measures are damaged; regardless, sentiment is helpful primarily at extremes.