{kind=link}

A reader asks:

What are we imagined to do over the subsequent 4 years with the Administration’s steady change in insurance policies? I went heavy into money earlier than Trump took workplace. I trusted that he was going to maintain his phrase, and break issues. I simply didn’t count on him to interrupt the market. However now I’m caught, petrified of this fixed uncertainty that appears to by no means go away. It’s already been a protracted 3 months. I used to be planning to retire this yr, however unlikely now. My Cash Market is getting that respectable 4% yield proper now, and at the very least this helps me sleep at night time.

One other reader asks:

I’m a 40 yr previous in good monetary place for the time being. That mentioned, I’m not bullish on the financial future. I’m not interested by hoarding gold bars, however wish to put a portion of my portfolio in investments that may do nicely, or at the very least higher, in a world the place revenue inequality, protectionism, AI advance, and America’s social material continues to fray. What would you advocate?

Every week I get a Google Doc filled with questions from our viewers at Ask the Compound.1

This was the collective sentiment from the questions this week:

There have been quite a few questions alongside the identical traces. Persons are anxious.

It’s loopy how shortly the narrative has shifted.

Just some brief months in the past there was speak of Trump being the most important pro-business, pro-stock market president ever:

Now persons are questioning if that is the tip of American exceptionalism:

Life comes at you quick.

If Trump retains up the present commerce insurance policies it’s going to be unhealthy for the worldwide financial system, provide chains, revenue margins, client costs and company earnings. There is no such thing as a sugar coating it. These usually are not pro-business or pro-stock market insurance policies. They’re the alternative.

However you’ll be able to’t simply go into the fetal place as a result of this makes you nervous. You continue to need to spend money on one thing.

These questions come from folks at completely different life levels, so I’ll deal with them individually.

Let’s say the worst does come to move and the subsequent few years are unhealthy for the financial system and the markets. Take away the rationale. The rationale doesn’t matter.

While you’re in retirement, you need to count on financial slowdowns, bear markets and corrections.

A pair retiring as we speak of their mid-60s has a 50-60% likelihood of at the very least certainly one of them residing till age 92. There might be a presidential election in 2028. That’s lower than 4 years away. Your retirement may final 20-30 years.

Until you have got an enormous pile of money, that cash market fund isn’t going that can assist you sustain with inflation over the approaching many years. You need to take some danger in retirement in case you want to beat the rise in lifestyle.

One of many huge dangers for retirement buyers is sequence of return danger. You don’t need unhealthy returns early in retirement to derail your funding plan. Due to this fact, you want to take into account what number of years’ value of spending you have got stashed away in secure, liquid property to see you thru the inevitable intervals of disruption. That’s true no matter who the president is.

Retirement planning nonetheless comes right down to your time horizon, monetary circumstances, and private spending habits. Uncertainty in retirement by no means goes away however you need to give attention to what you management and make course corrections to your plan alongside the best way.

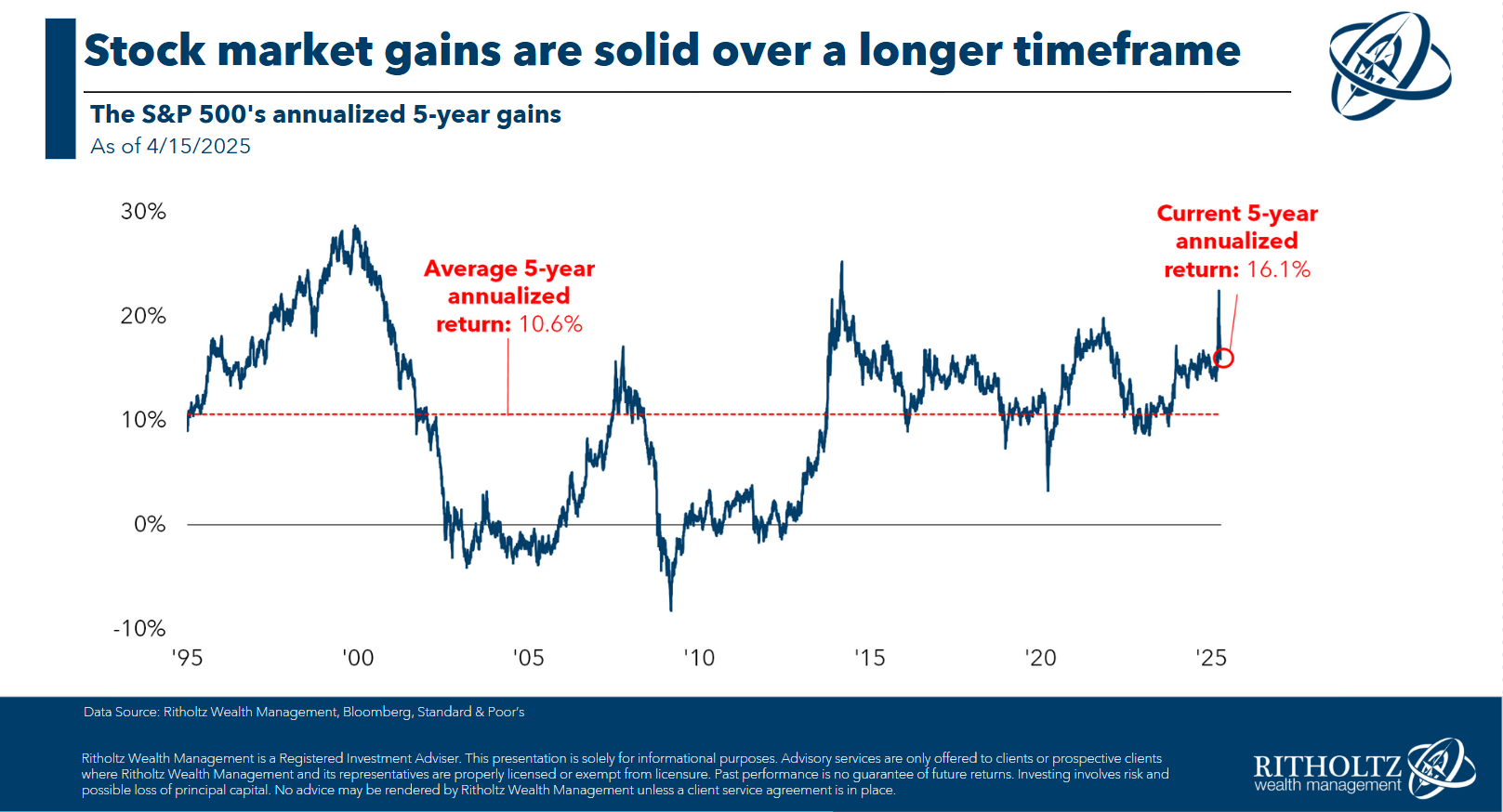

It’s additionally vital to acknowledge that inventory market returns have been implausible even while you embody the present correction:

Over the previous 5 years, the S&P 500 remains to be up 16% per yr.

The incorrect query: Ought to I promote all of my shares?

The best query: Ought to I alter my allocation?

When you’re 100% shares and this makes you that nervous perhaps you need to be extra like 80/20, 70/30 or 60/40. I’m by no means a fan of going all out with no plan on the opposite aspect of that call.

Asset allocation is extra vital than market timing.

Investing in center age is commonly missed since private finance consultants are inclined to give attention to younger buyers (keep the course) or retired buyers. At 40, it’s best to have some monetary property however you even have loads of time left to save lots of and make investments.

It’s a balancing act.

I don’t know if you need to be pessimistic about the way forward for our financial system however unhealthy occasions needs to be anticipated when you have got a multi-decade time horizon.

I broke down varied asset class returns by decade to get a way of efficiency throughout the tough stretches:

The unhealthy financial many years have been the Thirties, Seventies and 2000s. Shares carried out poorly in all three of these many years.2

Gold did fairly nicely in all of these intervals. Bonds held up nicely within the Thirties and 2000s however acquired crushed by inflation within the Seventies. Housing crashed throughout the Nice Despair however carried out phenomenally within the Seventies and 2000s.

Hear, I may provide you with a portfolio to guard your property with a bunch of various methods. Perhaps it really works, perhaps it doesn’t. The proper portfolio is just identified in hindsight.

These are the occasions when diversification issues greater than ever. It’s not solely a danger administration technique however a method to make sure you spend money on the eventual winners (which we received’t know till after the actual fact).

Your skill to stay with a technique might be extra vital than the technique itself.

When you’re actually that nervous in regards to the financial system, save extra money. Do your greatest to enhance your profession prospects and improve your revenue.

It’s additionally value declaring that predicting the long run is tough. Nobody would have anticipated issues to end up so nicely after Covid hit. Simply take a breath and see how this all performs out.

I’m not going to lie — I don’t have plenty of religion in our political leaders in both get together nowadays.

However I nonetheless think about the American spirit of ingenuity and entrepreneurship. I nonetheless have religion firms will do something they’ll to show a revenue and develop.

That hasn’t modified.

No matter you do along with your cash, simply have a plan in place and don’t let your feelings drive your funding selections.

Callie Cox joined me on Ask the Compound this week to debate these questions and far more:

Additional Studying:

Misbehaving in a Unstable Market

1E-mail us at askthecompoundshow@gmail.com if in case you have a query.

2Subtract inflation from the Seventies quantity and also you get destructive actual returns.