{kind=link}

One of many challenges that comes from analyzing markets and the financial system is simply how a lot “grey” there may be. Most information factors exist alongside a loud continuum, topic to future revisions. The meanderings above or beneath the pattern could also be simply noise, or the beginning of one thing extra ominous. Key reversals happen not often and are troublesome to identify in actual time.

Add to this the truth that markets are far much less correlated to the financial system than most individuals imagine. We impose our want for order and clear causation, which leads us to think about we perceive the current with far better readability than our historical past suggests (to say nothing of the long run).

The previous few months exemplify this:

Shopper sentiment is janky, but client spending stays strong. The labor market is much less tight than earlier than, however wages have elevated, at the same time as unemployment stays low. Inflation has fallenhowever is beginning to perk again up. Housing remains to be messy, with little stock and excessive mortgage charges. Company earnings are at file highs, and expectations are for continued progress.

Tariffs are the wild card.

Thus far, firms have absorbed a lot of the tariffs however are anticipated to begin passing these prices on to customers. Tariffs are a consumption tax, and at the very least up to now, they’ve solely had a light impact on spending. However it’s nonetheless early, and the Trump 2.0 tariff regime is prone to create modest headwinds for future client spending.

Then, there may be the V.O.S. Choices, Inc. v. Trump, which I mentioned in July. I stay stunned at how little protection this case has acquired, contemplating its potential to overturn ALL of the two.0 tariffs. If that have been to happen, it could be a bullish shock. (We are going to talk about this extra sooner or later if mandatory).

Final, there are the underlying technicals of the market: There appears to be countless liquidity, and markets have shaken off each little bit of dangerous information. (I’m extra within the response to the information than the information itself).

How a lot are these crosscurrents – client spending, labor, price cuts, inflation, housing, tariff coverage, and many others. – already mirrored in inventory costs? Contemplating that we’re presently buying and selling at all-time highs, the belief is that the markets are already discounting plenty of the dangerous information.

Traditionally, secular bull markets can run for much longer, additional, and better than most observers anticipate. The lengthy bull runs of 1982-2000 and 1946-1966 are prime examples. This secular bull run started in March 2013, when nearly each market broke out over its prior buying and selling vary. At 12 years outdated, it might nonetheless have a goodly variety of years left to run. The large Covid-19 fiscal stimulus continues to be a tailwind, even when it was a serious supply of inflation from 2020 to 2023. I do not know how that “reset” impacts market longevity, however I think it’s a vital issue.

Thus far, markets have climbed the wall of fear in 2025. The open query is how a lot costs have included massive upside or draw back surprises.

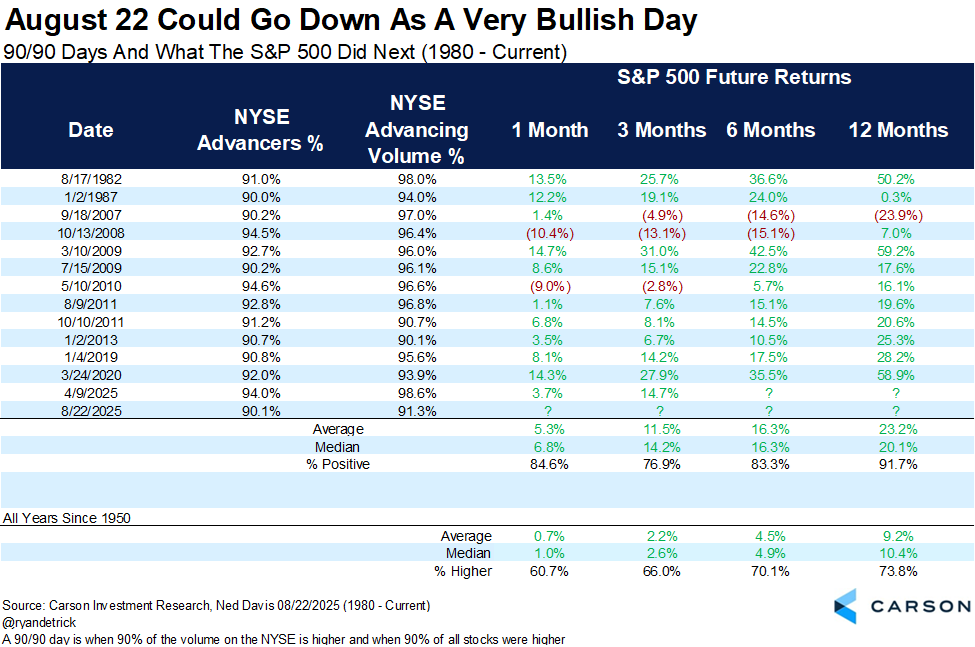

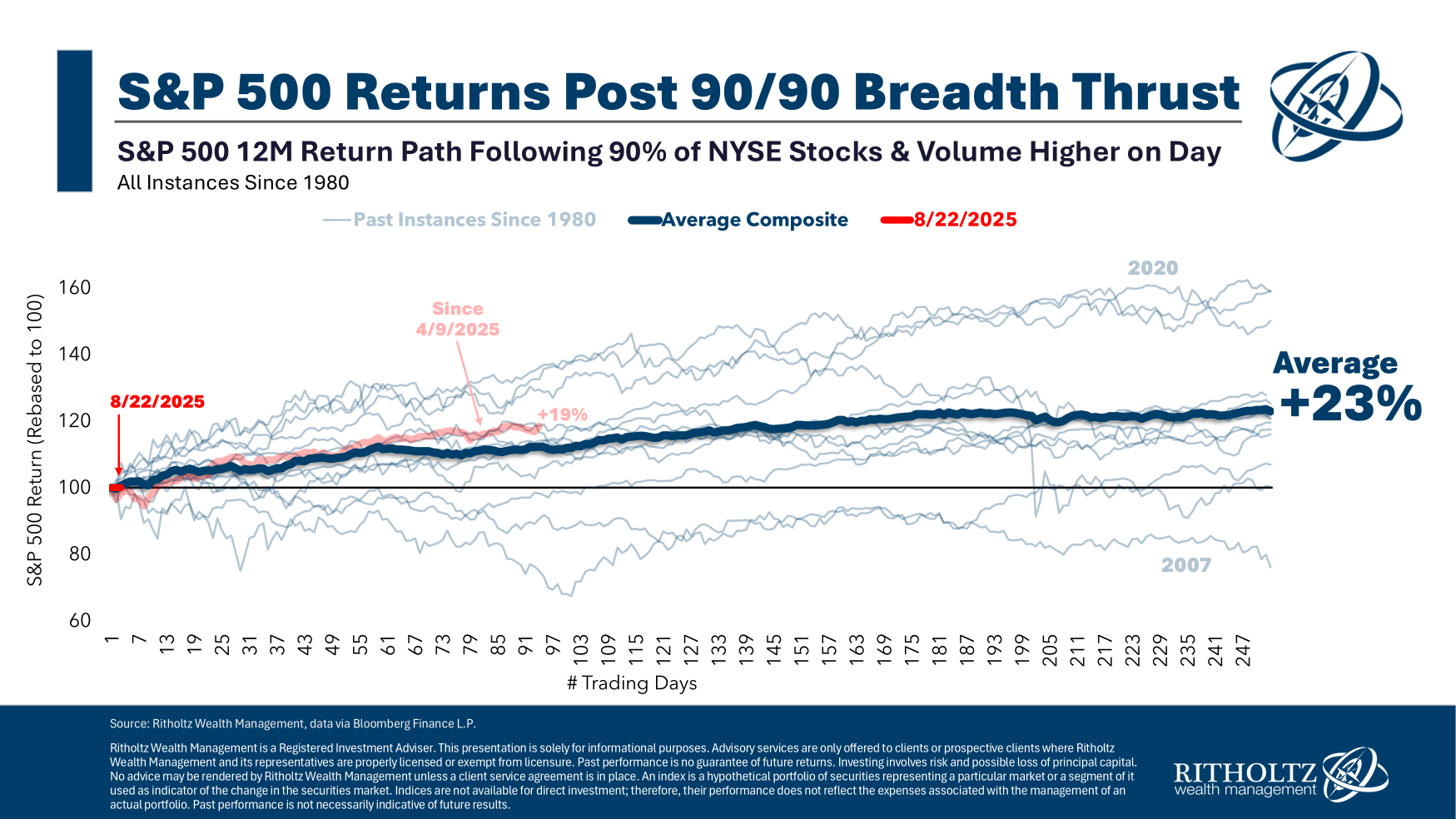

Take into account the thrust chart up high (desk beneath).

Once we see days like these, the place 90% of the quantity on the NYSE is larger, and 90% of all shares are within the inexperienced, it tends to be bullish for the following 12 months of good points. The final 90/90 day was April 9th of this yr, once we had a 90-day pause on Tariffs. The S&P 500 is up 29.8% since then; the Nasdaq 100 has gained 37.5%.

Since 1982, now we have seen one unfavorable, one flattish, and 12 constructive units of returns over the 12 months that adopted a 90/90 day. It’s not a assure, nevertheless it suggests favorable odds for remaining constructive.

See Additionally:

Will US inflation information assist investor hopes of a price lower? (Monetary Occasions, August 24, 2025)

How Lengthy Can This Uncanny Inventory Market Prosper? (New York Occasions, August 22, 2025)

Automobiles, espresso and clothes are poised to get pricier with new tariffs (Washington Publish, August 8 2025)

What’s the underside line? (Sam Ro, Aug 17, 2025)

Beforehand:

Would possibly Tariffs Get “Overturned”? (July 31, 2025)

The Muted Affect of Tariffs on Inflation So Far (July 17, 2025)

Are Tariffs a New US VAT Tax? (March 31, 2025)

NFP Disappoint; Revisions Worse (August 1, 2025)

The Magnificent 493 (August 12, 2025)

All Time Highs Are Bullish (June 26, 2025)

A Spectacularly Underappreciated 15 Years (April 28, 2025)

7 Growing Chances of Error (February 24, 2025)

What Is Driving Inflation? (July 29, 2025)